Why choose a Max Funded IUL Account?

Explore the Benefits of Indexed Universal Life and why savvy families are choosing to contribute to an IUL account over their 401k

Learn how to open an IUL Account & create generational wealth!

Is an IUL Account a good choice for you?

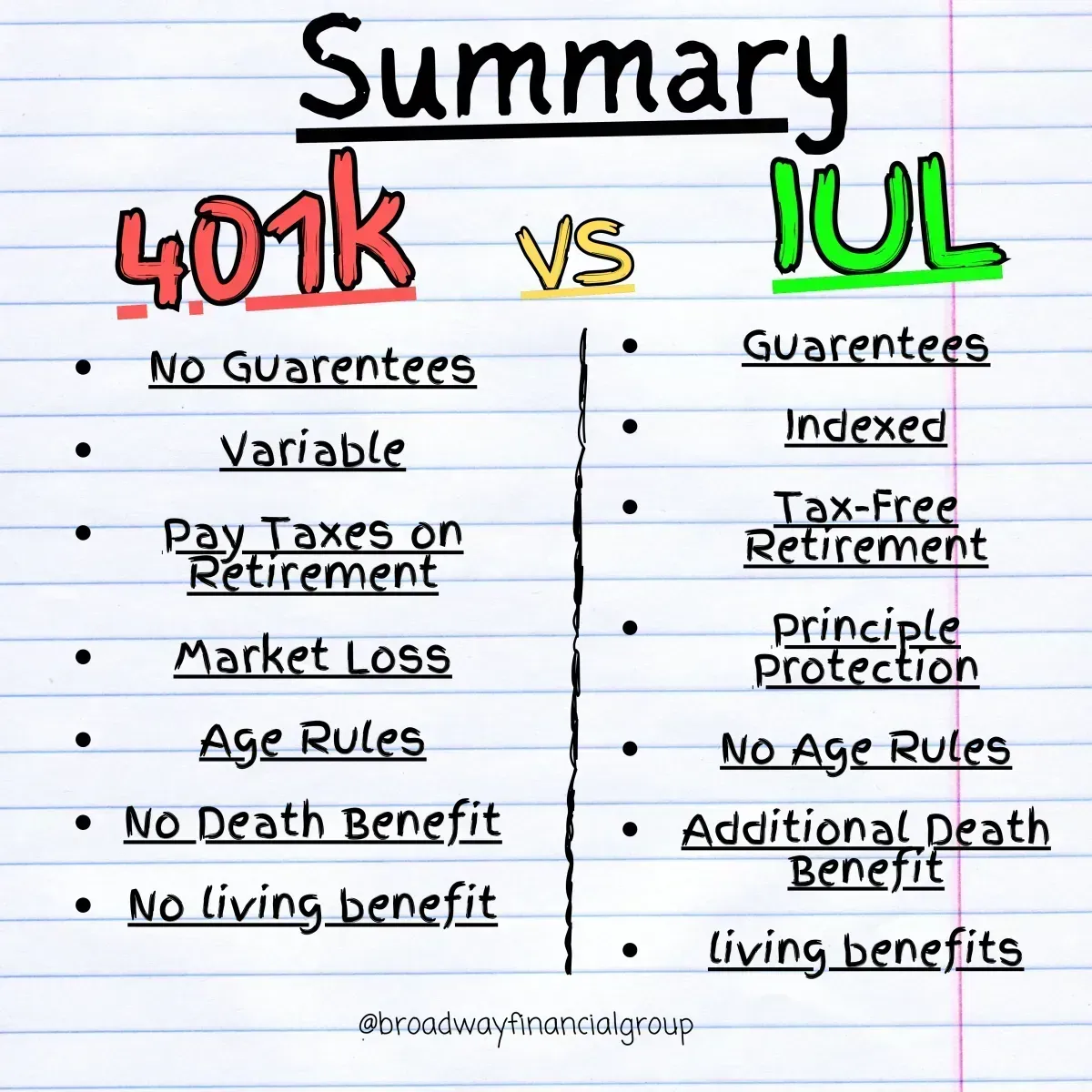

If you're seeking coverage that marries the flexibility of life insurance with a cash value account offering higher growth potential and protection from stock market loss, indexed universal life insurance might be worth a look.

However, IULs Accounts are NOT offered through Banks but instead, through Insurance Brokers.

Indexed universal life, or IUL, lets you tie your cash value to the performance of a stock or bond index without directly investing in the market.

IUL policies are straightforward and easy to understand. If you are a discerning investor looking for a vehicle that allows no limit on contributions, tax-free accumulation, allows tax free withdrawals anytime after the first year, and pays a tax-free death benefit when you pass away, an IUL could be the right choice for you.

When properly structured, IUL Plans serve as...

Tax-free Retirement

College Savings Plan

Becoming Your Own Bank

Infinite Banking

Guaranteed income

Leaving a Legacy (Creating Generational Wealth)

No early withdrawal penalties from the IRS

Safety in a Tier 1 Capital Asset (Similar to where banks keep their money)

Living Benefits whereby you don't have to lose your life to receive financial benefits

Evolution of the IUL...

1583 First Life Insurance policy, Royal Exchange, London.

1980 Universal life, EF Hutton.

1982 TEFRA established universal life as life insurance

1984 DEFRA placed specific limitations on premium size relative to an outstanding DB

1988 TAMRA specified a seven-pay test, whereby premiums paid into the policy cannot exceed the total amount that would be needed to have the policy fully paid in 7 years. .

1997 IUL created indexing.

Section 72(e): Explains how you can grow your money tax free.

Section 7702: Explains how you can pull money out tax free.

Section 101(a): Allows the death benefit to be paid out tax-free.

To see if you qualify, fill out the info below.

Accuracy is important!

**We value your privacy and are committed to protecting your personal information.**